핵심 요약:

- 초단기 국채 펀드, 2026년 3월 사상 최대 월간 유입 기록

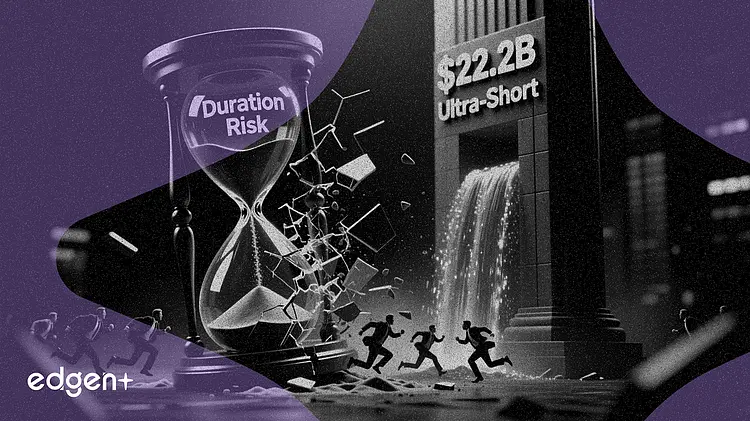

- 블랙록 0-3개월물 국채 ETF에 222억 달러 유입, 장기물 펀드에서는 32억 달러 이탈

- 자금 이동은 기간 회피 현상 반영, 채권 투자 자체의 철회는 아님

핵심 요약:

투자자들은 올해 블랙록의 0-3개월물 국채 ETF에 222억 달러를 쏟아부은 반면 장기물 ETF에서는 32억 달러를 인출했다. 이는 채권 매수자들이 만기 위험을 압축하고 있다는 가장 명확한 신호다.

연방준비제도(Fed)의 2% 목표치를 웃도는 지속적인 인플레이션으로 인해 투자자들은 기록적인 속도로 초단기 국채 펀드로 몰려들고 있다. 해당 카테고리는 3월에 사상 최대 월간 유입액을 기록했으며, 블랙록의 0-3개월물 국채 ETF는 연초 이후 222억 달러를 흡수했다.

"많은 사람들이 2022년에 겁을 먹었고 기간 위험을 원하지 않습니다. 단기물에서 대부분의 수익률을 얻을 수 있는데 굳이 위험을 감수할 필요가 있나요?"라고 모닝스타의 애널리스트 다니엘 소티로프는 말했다.

30년물 국채 수익률은 5월 19일 19년 만에 최고치를 기록했으며, 블랙록의 20년 이상물 국채 인덱스 펀드는 2월 28일 이스라엘-하마스 전쟁 확전 시작 이후 그 정점까지 9% 하락했다. 팩트셋에 따르면 이 펀드는 연초 이후 32억 달러의 자금 유출을 기록했다. 이와 대조적으로, 3개월물 국채 수익률은 약 3.6%로, 가격 민감도가 거의 없으면서도 유사한 소득을 제공한다.

이러한 자금 이동은 경기 침체 시 장기 국채가 주식 손실을 완충해줄 것으로 기대되는 전통적인 60/40 포트폴리오 모델에 도전장을 던지고 있다. 2021년 초 이후 소비자물가지수가 Fed의 목표를 상회하면서 이러한 헤지는 반복적으로 실패했다. "급등하는 국채 수익률은 전통적인 포트폴리오 분산 투자 수단이 어려움을 겪고 있다는 우리의 견해를 강조합니다"라고 블랙록 애널리스트들은 5월 26일 고객들에게 보낸 메모에서 밝혔다.

이러한 전환의 규모는 ETF 시장 전반에서 드러난다. iShares 0-3개월물 국채 ETF인 SGOV는 올해 뱅가드의 토털 본드 마켓 ETF와 같은 훨씬 더 큰 펀드들을 포함한 모든 채권형 ETF 중에서 가장 많은 자금을 유치했다. 이 펀드의 유효 듀레이션은 0.09년으로, 100베이시스포인트의 금리 변동 시 소득 효과 이전에 100달러 포지션 기준 약 0.09달러의 가격 변동을 의미하며, 이는 사실상 방향성 채권 베팅보다는 유동성 도구에 가깝다.

SPDR 블룸버그 1-3개월물 T-Bill ETF인 BIL은 SGOV의 0.09%보다 다소 높은 0.1353%의 비용 비율로 유사한 포트폴리오 목적을 수행한다. 두 펀드 모두 수익률 곡선의 최단기 구간에 위치하며, 투자자들이 단기 소득을 얻는 동시에 주식 밸류에이션이 재조정되거나 Fed의 정책 경로가 더 명확해질 경우 재배치할 수 있는 자본을 유지할 수 있게 해준다.

티커 BOXX로 알려진 Alpha Architect 1-3개월물 박스 ETF는 직접적인 국채 보유 대신 옵션 기반 박스 스프레드를 통해 국채 수익률과 유사한 수익을 추구하며 약 121억 달러 규모의 자산으로 성장했다. 옵션 만기까지의 평균 수익률은 약 4.2%이며, 순 비용 비율은 0.20% 미만이다. 이 펀드의 매력은 부분적으로 세금 효율성에 기반한다 — 수익의 상당 부분을 일반적인 이자 분배보다는 주가 상승을 통해 반영하려고 한다.

그러나 BOXX는 SGOV 및 BIL과 구조적으로 다르다. 투자 설명서는 일부 거래가 명확한 세금 지침을 갖추지 못할 수 있으며, 파생상품이 과세 대상 분배의 성격, 시기 및 금액에 영향을 미칠 수 있음을 인정한다. 최근 조사는 ETF 내 박스 스프레드 수익이 투자자들이 기대하는 세금 처리를 계속 받아야 하는지에 초점을 맞추고 있다. 이 펀드는 불리한 최종 결과 없이 운영되고 있지만, 많은 투자자들이 가치를 두는 세후 이점은 향후 해석 리스크에 직면할 수 있다.

2026년 자금 흐름의 광범위한 메시지는 투자자들이 채권 투자를 포기하고 있다는 것이 아니다. 그들은 듀레이션을 압축하고 있는 것이다. 단기물 수익률이 4%에 근접한 상황에서 머니마켓 펀드, 예금 증서 및 은행 예금과 경쟁력 있는 수준을 유지하면서도 일상적인 유동성과 최소한의 가격 변동성을 제공한다. 기회비용은 명확하다. 장기 금리가 급락할 경우 장기 국채가 SGOV와 BIL을 outperform할 것이다. 그러나 현재로서는 거시 환경이 유동적이고 단기인 국채 익스포저에 유리하며, 투자자들은 달러로 투표하고 있다.

이 문서는 정보 제공 목적으로만 작성되었으며 투자 조언을 구성하지 않습니다.