Markets Confusing? Ask Edgen Search.

Instant answers, zero BS, and trading decisions your future self will thank you for.

Try Search Now

COHR Stock Analysis: The AI Optical Supercycle Is Just Getting Started | Edgen

COHR Stock Analysis: The AI Optical Supercycle Is Just Getting Started | Edgen

David Hartley · March 18, 2026 · tech-ai / semiconductors · BUY $304

Summary

- Thesis: Coherent Corp. has transformed from a diversified industrial supplier into a high-growth AI infrastructure leader, with its Datacenter & Communications segment now driving 72% of revenue at 34% YoY growth

- Rating: Buy — Price target $304 (Bull Case), representing ~17% upside from $258.93

- Key catalyst: Datacenter book-to-bill exceeding 4x signals explosive near-term revenue visibility through calendar 2027

- Primary risk: Execution risk on 6-inch InP wafer ramp; customer concentration in hyperscale cloud providers

Macro & Sector Context: The AI Optical Arms Race

The global AI infrastructure buildout has entered a phase that is difficult to overstate. Microsoft has committed approximately $80 billion in calendar 2025 datacenter capital expenditure, Google has earmarked $75 billion, and Amazon is spending roughly $65 billion, with each company signaling sustained or accelerating budgets into 2027. This torrent of hyperscaler spending is not speculative; it is driven by enterprise demand for large language model inference, retrieval-augmented generation workloads, and multi-modal AI services that require exponentially more interconnect bandwidth between GPUs, switches, and storage tiers. The optical transceiver sits at the heart of this buildout. The datacenter optical components market, valued at approximately $14.2 billion in 2025, is projected to reach $37 billion by 2031, implying a 14.2% compound annual growth rate that may prove conservative if 1.6-terabit adoption accelerates ahead of current timelines.

The technology migration from 400G to 800G transceivers is now well underway, with 800G modules accounting for the majority of new hyperscaler orders. The next transition, from 800G to 1.6T, is expected to begin volume shipments in late calendar 2026, effectively doubling the dollar content per port and expanding the serviceable addressable market to an estimated $44 billion by 2030. This generational upgrade cycle is unusually compressed; prior transitions from 100G to 400G took roughly four years, while the 400G-to-1.6T arc may complete in under three. For component suppliers with vertically integrated manufacturing, this compression creates both opportunity and execution risk in roughly equal measure.

The broader semiconductor ecosystem provides a supportive backdrop. The CHIPS and Science Act continues to channel federal incentives toward domestic manufacturing, with Coherent's Sherman, Texas facility positioned to benefit from both direct subsidies and the reshoring preference embedded in hyperscaler procurement strategies. Unlike the consumer electronics cycle, which has shown signs of deceleration, the AI infrastructure segment operates on a distinct and still-accelerating demand curve that is largely independent of traditional PC and smartphone volumes.

Coherent's Transformation: From Industrial Conglomerate to AI Enabler

The appointment of Jim Anderson as CEO in June 2024 marked a strategic inflection point for Coherent Corp. Anderson, who previously led AMD's Computing and Graphics Group and served as CEO of Lattice Semiconductor, brought a Silicon Valley growth playbook to a company that had historically operated as a diversified industrial photonics business. Within his first year, Anderson restructured the organization from four segments into two: Datacenter and Communications, which houses the high-growth optical transceiver, laser, and switching businesses, and Industrial, which consolidates the legacy materials, aerospace, and silicon carbide operations. This simplification was not merely cosmetic. It refocused capital allocation, R&D prioritization, and management attention squarely on the AI opportunity, while providing transparency that the market had long demanded.

The strategic foundation for this transformation was laid by the 2022 merger of II-VI Incorporated and Coherent Corp., a $7 billion deal that created the only company in the optical supply chain with end-to-end vertical integration from raw indium phosphide and gallium arsenide crystal growth through epitaxial wafer fabrication, chip processing, and finished transceiver module assembly. CFO Sherri Luther has consistently highlighted on earnings calls that this vertical integration yields a 15-to-20 percentage point gross margin advantage over competitors who purchase key components on the merchant market. Board member Steve Skaggs, the former Lattice CEO who recruited Anderson, has been instrumental in shaping the capital allocation framework that prioritizes datacenter growth while maintaining optionality in silicon carbide for the EV power electronics market.

The cultural shift is evident in how the company communicates. Earnings calls under Anderson's leadership have become notably more forward-looking, with detailed commentary on design wins, customer engagement pipelines, and technology roadmaps that were previously absent. The company has also accelerated its deleveraging, reducing net debt from $4.2 billion at the time of the merger to approximately $3.1 billion as of the December 2025 quarter, with a stated target of reaching investment-grade credit metrics by mid-fiscal 2027. This balance sheet improvement widens the strategic aperture for both organic investment and potential tuck-in acquisitions in adjacent optical technologies.

Operating Performance: The Numbers Tell the Story

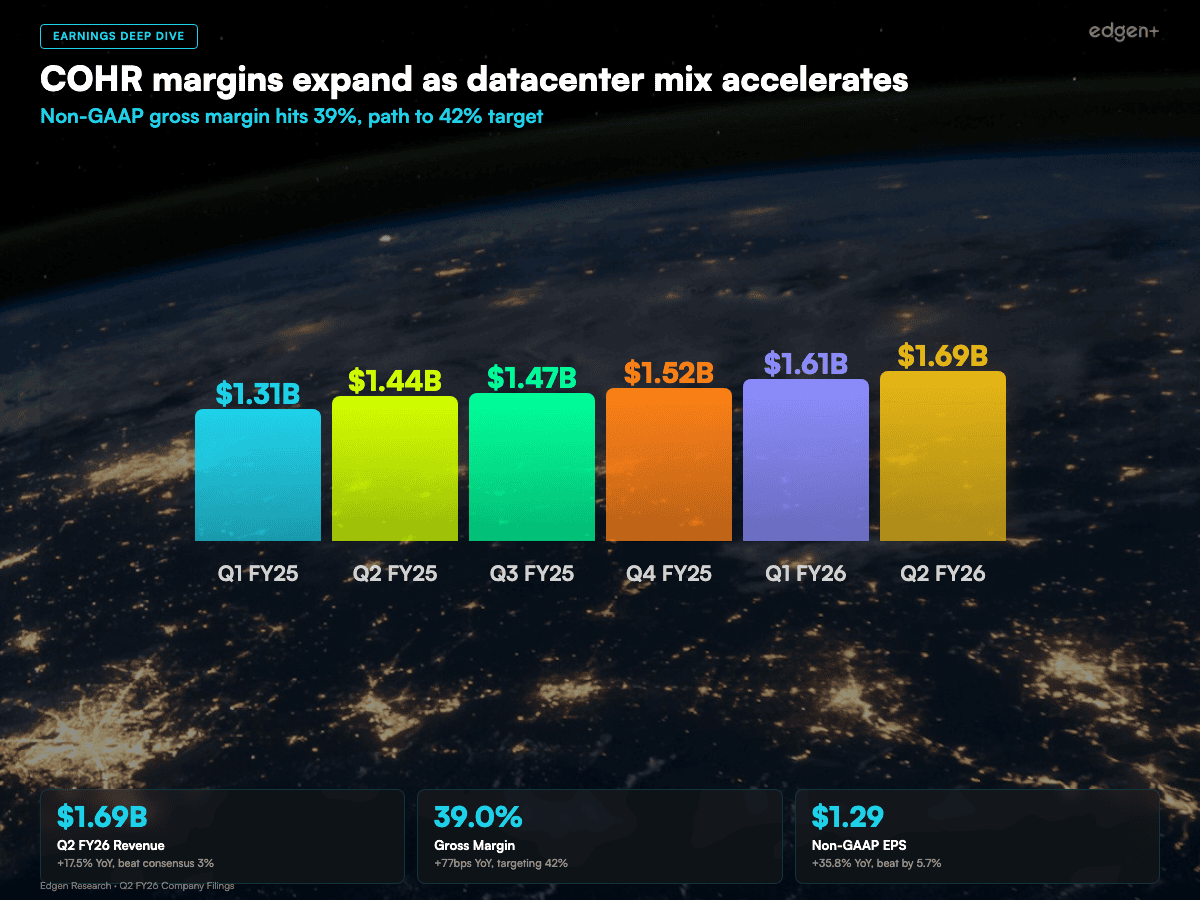

Coherent's second quarter of fiscal 2026, ending December 31, 2025, delivered results that exceeded expectations across every meaningful metric. Revenue reached $1.69 billion, a 17.5% increase year-over-year and a 4.7% sequential improvement that beat consensus estimates by approximately 3%. Non-GAAP earnings per share came in at $1.29, representing 35.8% growth over the prior-year quarter and surpassing analyst expectations by 5.7%. These are not marginal beats on lowered bars; the company has now exceeded consensus revenue estimates in six consecutive quarters, with the magnitude of the beat widening in each of the last three.

The segment-level performance reveals the dual narrative that defines Coherent today. The Datacenter and Communications segment generated $1.21 billion in revenue, a 34% year-over-year increase that pushed the segment to 72% of total company revenue, up from 63% in the year-ago quarter. The book-to-bill ratio for datacenter products exceeded 4.0x in the quarter, a figure that Anderson described as "unprecedented" and one that provides revenue visibility extending well into calendar 2027. On the other side, the Industrial segment reported $478 million in revenue, a 10% year-over-year decline reflecting continued cyclical weakness in telecom infrastructure, automotive silicon carbide, and legacy industrial laser markets. Management expects this segment to trough in the March 2026 quarter before a modest recovery begins in the second half of the fiscal year.

Margin expansion is tracking ahead of the internal roadmap. Non-GAAP gross margin reached 39.0%, an improvement of 77 basis points year-over-year, driven by favorable datacenter mix, improving yields on 800G transceiver production, and early benefits from the 6-inch indium phosphide wafer transition. Non-GAAP operating margin expanded to 19.9%, a 147 basis point year-over-year improvement that reflects operating leverage on higher volumes and disciplined expense management. For the third quarter of fiscal 2026, management guided revenue to a range of $1.70 billion to $1.84 billion and non-GAAP EPS of $1.28 to $1.48, implying continued sequential improvement. The midpoint of EPS guidance suggests the path to Coherent's medium-term target of 42% gross margins and 25% operating margins is credible, though it requires flawless execution on the next-generation product ramp.

Source: Company filings. COHR revenue ($B) and gross margin (%).

The 1.6T Transition and Next-Gen Product Ramp

The transition from 800G to 1.6T transceivers represents the single most important product cycle for Coherent over the next 18 months. The company's 1.6T transceiver platform, which integrates proprietary indium phosphide electro-absorption modulated lasers with advanced digital signal processing, is currently sampling with all major hyperscaler customers and is on track for volume production in the second half of calendar 2026. The 1.6T module carries approximately 1.8x the average selling price of an 800G unit while requiring only modestly more manufacturing complexity, creating a powerful margin tailwind as the mix shifts. Anderson has indicated that Coherent expects to hold or gain share in the 1.6T generation relative to its current 800G position, a claim supported by the company's early sampling timelines and the deep co-engineering relationships with customers that vertical integration enables.

The 6-inch indium phosphide wafer ramp at the Sherman, Texas facility is the linchpin of Coherent's cost structure for the next three years. Moving from 3-inch to 6-inch wafers yields approximately 4x the number of usable devices per wafer, translating to a projected 60% reduction in per-device cost at mature yields. This is not merely an incremental improvement; it is a structural cost advantage that no competitor has yet replicated at scale. Lumentum is investing in similar technology but remains approximately 12 to 18 months behind Coherent's timeline, while Chinese competitors such as Innolight and Eoptolink rely on purchased InP chips and therefore cannot capture this vertical integration benefit. The first production-qualified 6-inch wafers are expected to enter the supply chain in the June 2026 quarter, with full ramp extending through fiscal 2027. Yield data from this transition will be the single most important variable to monitor in coming earnings reports.

Beyond transceivers, Coherent is building optionality in two adjacent technologies that could meaningfully expand its addressable market. Co-Packaged Optics, which integrates optical engines directly onto switch ASICs to reduce power consumption and latency, has progressed from concept to commercial reality. The company disclosed a "large purchase order" from a leading AI datacenter customer for CPO components, validating the technology's readiness and Coherent's positioning. Optical Circuit Switching, which enables dynamic reconfiguration of datacenter network topology without electronic packet processing, represents an earlier-stage but potentially transformative opportunity. Coherent has more than 10 active customer engagements for its OCS platform, targeting a market that industry analysts project could reach $2 billion or more by 2030. Neither CPO nor OCS is priced into current consensus estimates, providing upside optionality that the market has not yet fully appreciated.

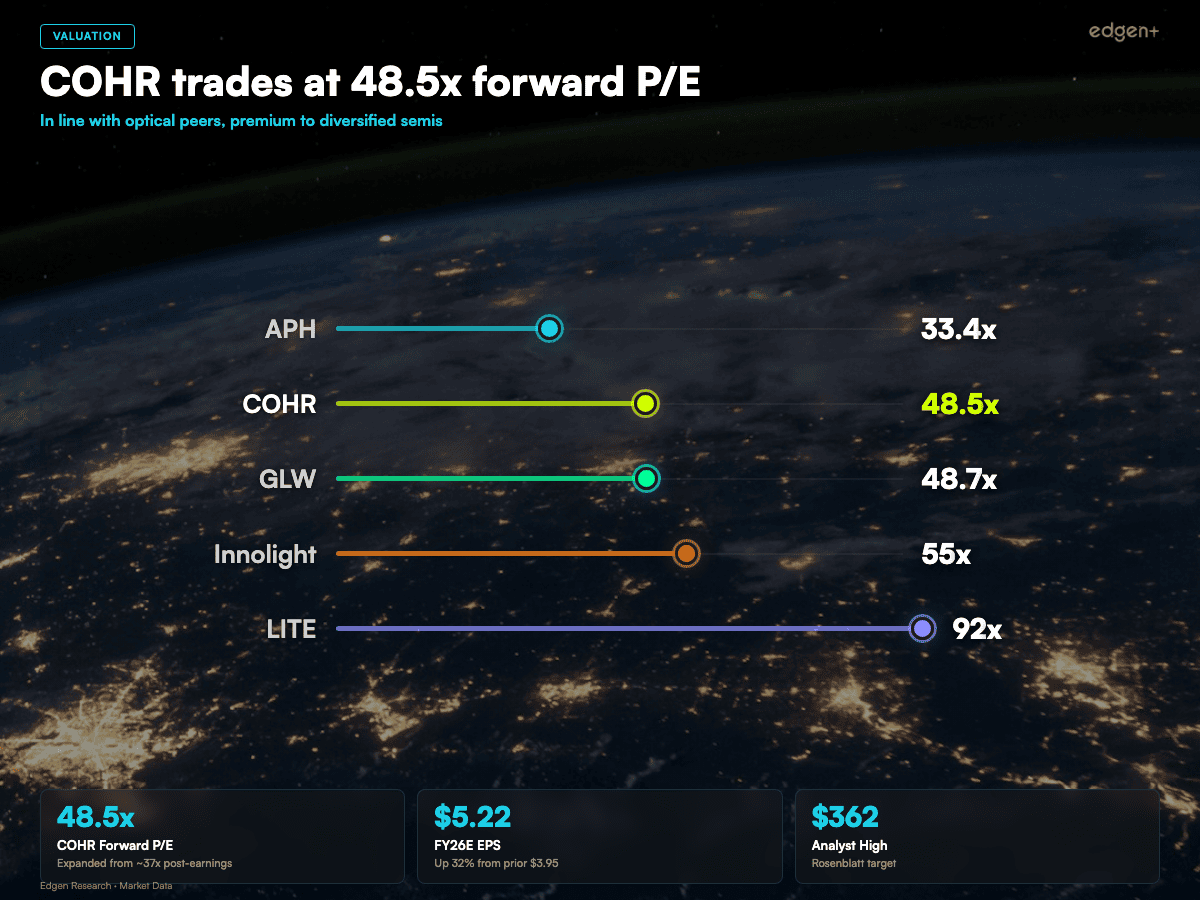

Source: Market data, consensus estimates. COHR valuation range analysis.

Valuation: Premium Justified by Growth Acceleration

Coherent trades at approximately 48.5x forward earnings based on consensus fiscal 2026 EPS of $5.22, a multiple that has expanded from roughly 37x just weeks ago as the market digests the magnitude of the datacenter backlog. This valuation demands scrutiny but holds up well in context. Lumentum Technologies trades at 92x forward earnings on the back of its own record backlog disclosure, while Chinese competitor Innolight commands approximately 55x despite lower margins and no vertical integration. Among diversified peers, Amphenol trades at 33.4x and Corning at 48.7x. Coherent's multiple sits comfortably below its pure-play optical peers and roughly in line with Corning, a company growing revenue at less than half Coherent's rate. The premium to Amphenol reflects Coherent's significantly higher revenue growth trajectory and its direct exposure to the highest-growth segment of AI infrastructure.

Consensus estimates have moved sharply higher over the past six months. Fiscal 2026 EPS expectations have risen from approximately $3.95 to $5.22, a 32% upward revision that reflects both operational outperformance and improved forward guidance. Fiscal 2027 consensus stands at $6.69, and fiscal 2028 at $8.17, implying a three-year EPS compound annual growth rate of approximately 25%. Revenue is projected to grow at roughly 20% annually over the same period, driven almost entirely by the datacenter segment. On a PEG basis, Coherent's ratio of approximately 1.9x compares favorably to the optical peer group average of 2.4x, suggesting that the stock is not overvalued relative to its growth rate despite the headline multiple appearing rich.

Wall Street analyst price targets span a wide range, from a low of $170 to a high of $362.25, with a median of $255. The current share price of $258.93 sits slightly above the median target, which reflects the rapid appreciation following the Q2 earnings report and backlog disclosure. Our quality score assessment highlights several strengths: top-decile revenue growth, expanding margins with a credible path to targets, improving balance sheet leverage, and a management team with a proven track record of execution. The primary quality concern is the concentration of growth in a single end market, which compresses the margin of safety in any downside scenario.

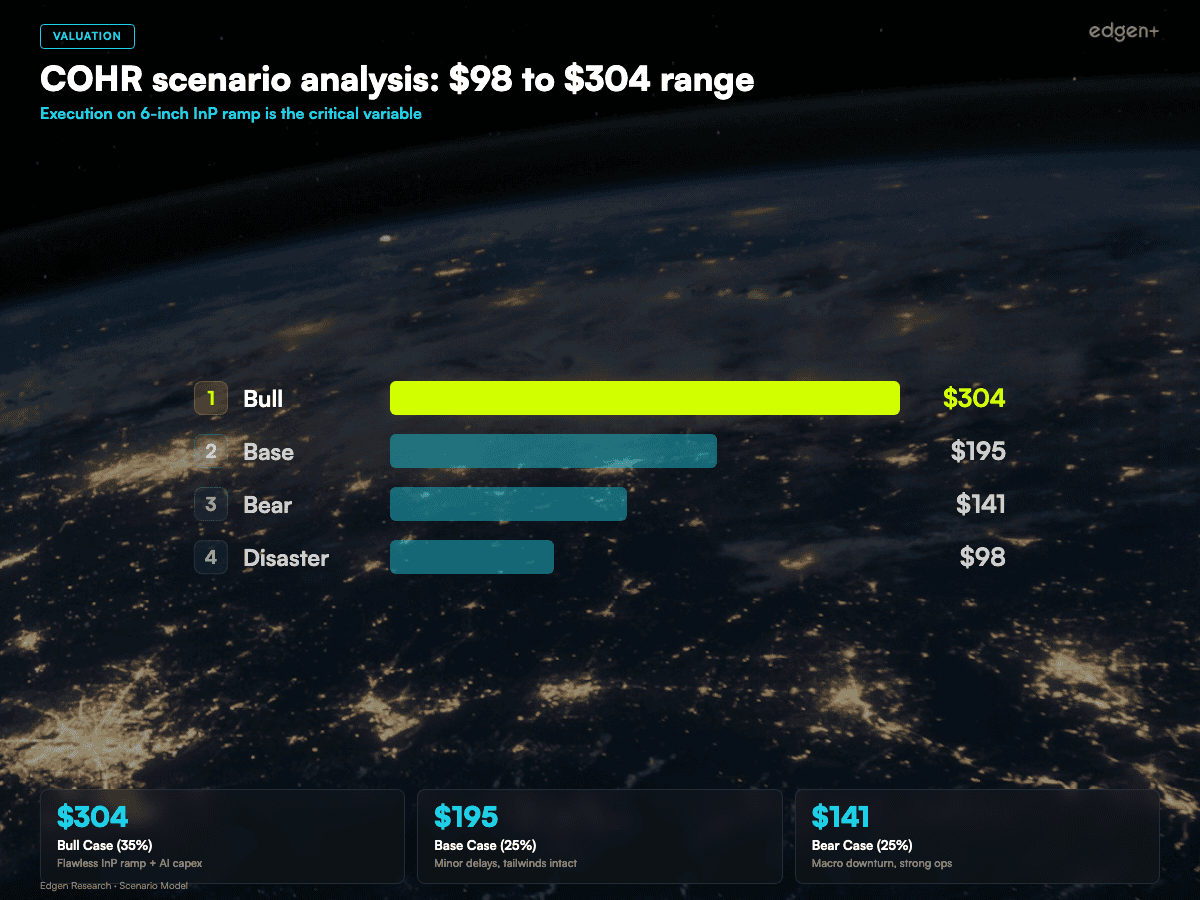

Three Scenarios

Scenario | Price Target | Market Cap | Probability | Key Assumption |

**Bull** | $304 | ~$57B | 35% | Flawless InP ramp + AI capex continues + 1.6T/CPO wins |

**Base** | $195 | ~$36.5B | 25% | Minor execution delays, sector tailwinds intact |

**Bear** | $141 | ~$26.4B | 25% | Macro downturn compresses multiples despite strong ops |

**Disaster** | $98 | ~$18.4B | 15% | InP ramp failure + hyperscaler spending pause |

Source: Edgen Research estimates. COHR three-scenario valuation.

Risks and Bear Case

Execution Risk on InP Capacity Expansion. The 6-inch indium phosphide wafer transition at Coherent's Sherman, Texas facility is a technically demanding process that has never been executed at this scale in the industry. Moving from 3-inch to 6-inch substrates requires new crystal growth techniques, modified epitaxial deposition parameters, and recalibrated lithography processes, any of which could produce yield shortfalls that delay volume production by one to three quarters. If yields on 6-inch wafers plateau at 70% rather than reaching the targeted 90%+ within the first 12 months, the projected 60% cost reduction would shrink to approximately 35%, undermining the gross margin expansion thesis and potentially causing Coherent to miss its 42% gross margin target by 200 or more basis points. Anderson and Luther have both acknowledged this risk on recent calls, noting that the company has built schedule buffer into its internal timeline, but investors should recognize that no amount of management confidence eliminates the fundamental physics and engineering challenges involved in scaling compound semiconductor wafer diameters.

Customer Concentration in Hyperscale Cloud Providers. With the Datacenter and Communications segment now generating 72% of total revenue and the top three hyperscaler customers likely accounting for 50% or more of that segment, Coherent's revenue base is concentrated to a degree that creates binary risk. A decision by any single hyperscaler to dual-source more aggressively, to delay a datacenter buildout by even two quarters, or to bring optical transceiver design in-house, as Google has explored with its custom TPU interconnects, could remove hundreds of millions of dollars in expected revenue with limited offset from other customers. The 4x book-to-bill ratio, while impressive, is itself a reflection of this concentration; orders from three to four customers drive the vast majority of the backlog. History offers cautionary precedent: in 2019, a single hyperscaler's inventory correction triggered a 30% revenue decline at several optical component suppliers within two quarters. Coherent's diversified Industrial segment provides a partial buffer, but at only 28% of revenue and declining, it cannot absorb a meaningful datacenter shortfall.

Competitive Pressure from Established and Emerging Rivals. Lumentum Technologies reported its own record backlog in January 2026 and is investing aggressively in next-generation transceiver platforms that could challenge Coherent's share gains in 1.6T. More concerning is the competitive threat from Chinese manufacturers Innolight and Eoptolink, which together hold approximately 60% of the 800G merchant transceiver market and benefit from structurally lower labor costs, favorable government subsidies, and proximity to Asian contract manufacturers. While Coherent's vertical integration provides a durable cost advantage at the component level, Chinese competitors have demonstrated the ability to close technology gaps within 12 to 18 months of initial product launches and to compete aggressively on price in ways that compress margins across the entire supply chain. If the 1.6T transition commoditizes faster than the 800G cycle did, Coherent's premium valuation could come under pressure even if the company executes flawlessly on its technology roadmap.

Conclusion and Price Target

Coherent Corp. is executing on one of the most powerful secular growth stories in the semiconductor and photonics industry. The convergence of hyperscaler AI capital expenditure, the 800G-to-1.6T transceiver upgrade cycle, and the emerging CPO and OCS opportunities creates a multi-year revenue tailwind that few companies are as well positioned to capture. Under CEO Jim Anderson's leadership, the strategic transformation from industrial conglomerate to AI infrastructure pure-play has been decisive and effective, with operational results consistently exceeding expectations and the balance sheet improving at an accelerating pace. The 4x-plus book-to-bill ratio in datacenter provides a level of forward revenue visibility that is genuinely rare in the technology hardware sector.

We rate Coherent Corp. a Buy with a price target of $304, our Bull Case scenario, representing approximately 17% upside from the current share price of $258.93. This target assumes successful execution on the 6-inch InP wafer ramp, continued hyperscaler capital expenditure at or above current run rates, and share gains in the 1.6T and CPO product cycles. The probability-weighted expected value across our four scenarios is approximately $207, which sits below the current price and reflects the meaningful tail risk embedded in the Disaster scenario. However, we believe the Bull Case probability is understated by the market, particularly given the backlog visibility and the structural advantages of vertical integration that are not easily replicated.

One thing to watch above all else: the 6-inch InP wafer yield data that will begin to surface in Coherent's fiscal Q4 2026 and Q1 2027 earnings reports. This single variable will determine whether gross margins reach the 42%+ target that underpins both the Bull and Base Case scenarios, and it will validate or invalidate the core thesis that vertical integration in compound semiconductors creates a durable, widening competitive moat. Investors with a 12-to-18-month horizon and tolerance for the execution risk inherent in a technology transition of this magnitude should find Coherent's risk-reward profile compelling at current levels.

Internal Links

- COHR Stock Forecast and Price Target

- AI Optical Sector Deep Dive: COHR vs LITE vs GLW

- LITE Stock Analysis

Frequently Asked Questions

Is COHR stock a good buy right now?

Coherent Corp. is rated Buy with a $304 price target, representing approximately 17% upside from the current price of $258.93. The primary catalyst is a datacenter book-to-bill ratio exceeding 4x, which provides revenue visibility through calendar 2027 and signals that the AI optical infrastructure buildout is accelerating rather than peaking. Investors should weigh this upside against execution risk on the 6-inch InP wafer ramp and customer concentration in hyperscale cloud providers.

What is Coherent Corp's price target for 2026?

Wall Street analyst price targets for COHR range from $170 at the low end to $362.25 at the high end, with a median of $255. Our price target is $304, based on a Bull Case scenario that assumes successful execution on the 1.6T transceiver ramp, continued hyperscaler CapEx growth, and gross margin expansion toward the 42% target driven by the 6-inch InP wafer transition at the Sherman, Texas facility.

What are the main risks for COHR stock?

The three primary risks are execution risk on the 6-inch indium phosphide wafer ramp, which could delay cost reductions if yields underperform; customer concentration, with over 70% of revenue tied to datacenter customers and the top three hyperscalers representing a disproportionate share of the backlog; and competitive pressure from Lumentum, Innolight, and Eoptolink, which are investing aggressively in next-generation transceivers and could compress margins across the optical supply chain.

How does COHR compare to LITE and GLW?

Coherent trades at approximately 48.5x forward earnings, compared to Lumentum at 92x and Corning at 48.7x. Coherent offers a higher datacenter revenue growth rate of 34% year-over-year versus Lumentum's improving but historically lower optical communications growth, while Corning's optical segment grows at roughly half Coherent's rate. Coherent's unique advantage is end-to-end vertical integration from InP crystal growth through finished transceivers, a capability neither LITE nor GLW can match.

What is Coherent Corp's revenue growth rate?

Coherent reported Q2 FY26 revenue of $1.69 billion, representing 17.5% year-over-year growth on a reported basis and approximately 22% on a pro-forma basis adjusting for divestitures. The Datacenter and Communications segment grew 34% year-over-year to $1.21 billion, while the Industrial segment declined 10% due to cyclical weakness. Consensus projects total revenue to grow at approximately 20% annually over the next three years, driven almost entirely by datacenter demand.

Not financial advice. For educational and research purposes only.

Recommend