Markets Confusing? Ask Edgen Search.

Instant answers, zero BS, and trading decisions your future self will thank you for.

Try Search Now

LITE Stock Analysis: NVIDIA-Backed Optical Leader at a Crossroads | Edgen

LITE Stock Analysis: NVIDIA-Backed Optical Leader at a Crossroads | Edgen

David Hartley · March 18, 2026 · tech-ai / semiconductors · HOLD $633

Summary

- Thesis: Lumentum has transformed into a primary AI infrastructure enabler with explosive 65.5% revenue growth, validated by a $2B NVIDIA strategic investment and imminent S&P 500 inclusion — but the 84x forward P/E prices in perfection

- Rating: Hold — Price target $633 (near median analyst target), current price ~$625 offers limited near-term upside given elevated expectations

- Key catalyst: Q3 FY26 earnings (early May 2026) must validate $780-830M revenue guidance and 30-31% operating margins

- Primary risk: Operational execution on InP capacity ramp; 84x forward P/E leaves zero room for disappointment

Macro & Sector Context: The Optical Bottleneck in AI Infrastructure

The artificial intelligence revolution has created an infrastructure problem that silicon alone cannot solve. Every large language model training run, every inference cluster, every hyperscale data center expansion demands exponentially more bandwidth between chips, between racks, and between facilities. AI-optimized data centers require roughly ten times more optical interconnects than their traditional counterparts, and the industry is struggling to keep pace. The Cloud and Networking total addressable market stood at approximately $20.25 billion in 2025 and is projected to reach $28.65 billion by 2030, representing a 7.19% compound annual growth rate. Meanwhile, the 5G optical transceiver market tells an even more aggressive story, growing from $2.35 billion to an estimated $10.41 billion by 2031 at a 28.1% CAGR, as telecom operators upgrade backhaul and fronthaul networks to handle surging data traffic.

The supply-demand imbalance is acute. Hyperscaler capital expenditure — led by Microsoft, Meta, Google, and Amazon — is accelerating into 2026 and 2027, driving what can only be described as insatiable demand for electroabsorption modulated lasers (EMLs) and indium phosphide (InP) components that form the backbone of high-speed optical links. Lumentum management has publicly acknowledged that the company is under-shipping demand by approximately 30%, meaning order books are fuller than production lines can accommodate. This is both a validation of the technology's criticality and a warning about the execution challenge ahead.

The technology upgrade cycle compounds the demand picture. The industry is in the midst of transitioning from 100G and 200G optical modules to 800G transceivers, with 1.6T modules entering qualification at major cloud customers. Each generational leap requires more sophisticated photonic components — more laser sources, more complex modulation, tighter manufacturing tolerances — and the number of suppliers capable of producing at scale narrows with each step up. This is the structural tailwind behind Lumentum's reinvention, and it explains why NVIDIA chose to invest $2 billion in the company rather than build optical capabilities from scratch.

Lumentum's Reinvention: From Telecom Legacy to AI Powerhouse

Two years ago, Lumentum was a declining telecom components maker nursing margin compression and a shrinking backlog. Today it is the fastest-growing name in AI optical infrastructure, and the transformation is attributable to a combination of aggressive M&A, executive overhaul, and fortunate timing. CEO Michael Hurlston, appointed in February 2025 after stints leading Synaptics and holding senior roles at Finisar and Broadcom, brought a systems-level perspective to a company that had historically sold discrete components. Under his leadership, and with CFO Wajid Ali managing the balance sheet through a period of heavy investment, Lumentum executed two acquisitions that reshaped its competitive position: NeoPhotonics for $918 million in 2022, which added coherent DSP and silicon photonics design expertise, and Cloud Light for $750 million in late 2023, which moved the company from selling bare components into fully assembled transceiver modules. The result is a vertically integrated platform that spans lasers, modulators, receivers, and complete pluggable optics — a rare capability in the industry.

The business now operates in two segments, and the revenue mix tells the strategic story clearly. Cloud and Networking accounted for more than 88% of total revenue in Q2 FY26, generating $665.5 million in the quarter and growing at a pace that dwarfs everything else in the optical supply chain. The Industrial Tech segment — which includes 3D sensing, industrial lasers, and legacy telecom products — continues to decline and is increasingly irrelevant to the investment thesis, though Board Chair Penelope Herscher has noted in recent calls that the segment provides diversification during cyclical downturns. The real headline, however, is the NVIDIA partnership announced in March 2026: a $2 billion strategic investment via convertible preferred stock that positions Lumentum as a preferred co-developer for optical interconnects in NVIDIA's next-generation networking platforms, including Spectrum-X and Quantum-X switches. Separately, Lumentum's inclusion in the S&P 500 index, effective March 23, 2026, will trigger structural buying from index funds and ETFs that collectively manage trillions of dollars, creating a near-term demand floor under the stock. The company has paused share buybacks to fund its capacity expansion and M&A integration, a disciplined capital allocation decision given the growth runway ahead.

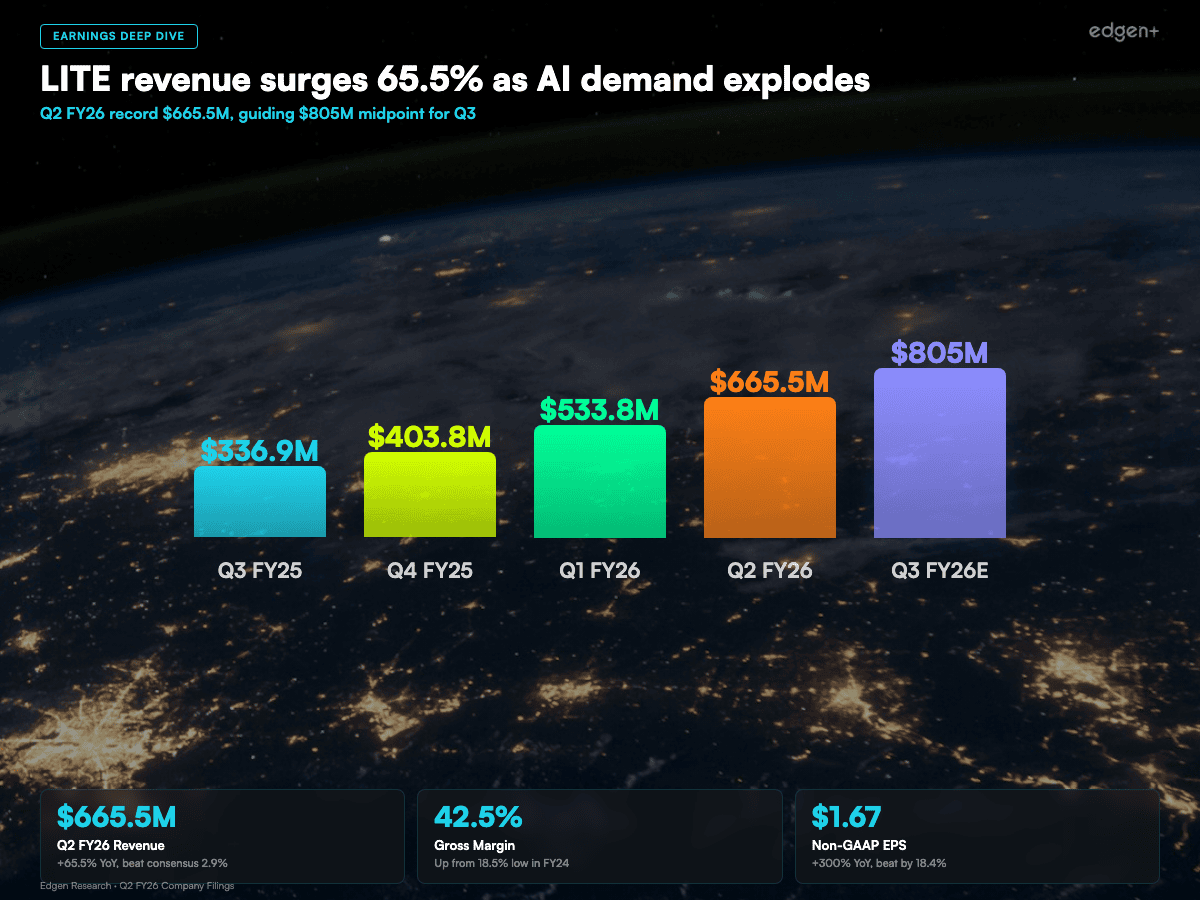

Operating Performance: Record-Breaking Acceleration

Lumentum's Q2 FY26 results, for the quarter ended December 27, 2025, were exceptional by any standard. Revenue reached $665.5 million, a 65.5% increase year-over-year that beat the Wall Street consensus estimate of $646.74 million by 2.9%. Non-GAAP earnings per share came in at $1.67, representing approximately 300% growth over the prior-year period and exceeding the consensus estimate of $1.41 by 18.4%. The Cloud and Networking segment delivered the entirety of the revenue upside, with components revenue at $443.7 million and systems revenue at $221.8 million, both records. The margin recovery has been equally dramatic: non-GAAP gross margin expanded to 42.5% in the quarter, up from a trough of just 18.5% during the depths of the telecom downturn in fiscal 2024, while operating margin reached 25.2% compared to a mere 3.0% in Q1 FY25.

The forward guidance is where the story gets both exciting and dangerous. Management guided Q3 FY26 revenue to a range of $780 million to $830 million, implying year-over-year growth in excess of 85%, with operating margins expanding further to 30-31%. CEO Michael Hurlston stated on the earnings call that demand is "far outstripping supply" and that the company is under-shipping customer requirements by roughly 30%. The book-to-bill ratio sits "firmly above one," with the OCS (Optical Connectivity Solutions) platform alone carrying a backlog exceeding $400 million. InP wafer fab capacity is fully subscribed through the end of calendar 2025, and new capacity in the United States, United Kingdom, and Japan is being brought online as rapidly as equipment lead times allow.

The trajectory from $665 million in Q2 to a guided midpoint of $805 million in Q3 implies a quarterly sequential acceleration of 21%, a rate that, if sustained, would put Lumentum on track for approximately $2.9 billion in full-year FY26 revenue and $4.62 billion in FY27. These are not small numbers for a company that generated $1.36 billion in all of fiscal 2025. The operating leverage inherent in the model — fixed fab costs spread over rapidly growing volumes — means that each incremental dollar of revenue falls to the bottom line at an increasingly favorable rate. The question is whether execution can keep pace with ambition.

Source: Company filings. LITE revenue ($B) and gross margin (%).

The NVIDIA Validation and S&P 500 Catalyst

The single most significant development in Lumentum's recent history is NVIDIA's $2 billion strategic investment, announced in March 2026 and structured as convertible preferred stock. This is not a passive financial investment. NVIDIA has designated Lumentum as a preferred co-development partner for optical interconnect technology that will be integrated into NVIDIA's silicon photonics ecosystem, specifically the Spectrum-X Ethernet switching platform and the Quantum-X InfiniBand platform that together form the networking backbone of the world's largest AI training clusters. The investment provides Lumentum with capital to accelerate its InP capacity buildout and next-generation product development, while giving NVIDIA a guaranteed supply of the photonic components it cannot easily source elsewhere. For investors, the NVIDIA imprimatur serves as a powerful signal of technology validation — Jensen Huang does not write $2 billion checks lightly.

The S&P 500 inclusion, effective March 23, 2026, adds a separate and mechanistically predictable catalyst. Index funds tracking the S&P 500 must purchase Lumentum shares to match the benchmark, creating a one-time wave of structural demand that typically supports the stock price in the weeks surrounding the effective date. With Lumentum's market capitalization now exceeding $40 billion, the index weighting will be meaningful, and passive fund flows should provide a near-term floor under the stock regardless of short-term earnings noise.

The product pipeline reinforces the strategic narrative. Lumentum's OCS platform has a backlog exceeding $400 million, including a multi-hundred-million-dollar co-packaged optics (CPO) purchase order that represents one of the largest single optical contracts in the industry's history. The company has begun shipping 1.6T transceiver samples to lead customers, positioning it at the forefront of the next generational upgrade. Its External Laser Source (ELS) modules for CPO architectures are in qualification at multiple hyperscalers. With more than 3,100 patents and a first-to-market position in 800G ZR+ coherent transceivers, Lumentum holds a technology moat that would take competitors years to replicate. The 12-month stock return of 862% — from a low of $45.65 to a high of $783.80 — reflects the market's recognition of this transformation, though it also raises the question of how much future growth is already embedded in the share price.

Valuation: The Growth Premium Debate

This is where the Lumentum story demands intellectual honesty. The stock trades at approximately 84 times forward earnings, a multiple that is dramatically higher than peers Coherent (COHR) at 48.5 times and Corning (GLW) at 49 times. On an enterprise-value-to-sales basis, the gap is even more pronounced: Lumentum commands a multiple north of 21 times, compared to 7.3 times for Coherent and 9.3 times for Marvell Technology, another key player in the AI networking chain. These are not small differences — Lumentum is priced at roughly double the valuation of its closest competitor on nearly every metric, and the market is implicitly assuming that the company will sustain growth rates and margin expansion that no optical company has ever delivered over a multi-year period.

The bull case for the valuation rests on the earnings trajectory. Consensus estimates project FY26 non-GAAP EPS of approximately $7.57, representing 270% growth over FY25's $2.06. Looking further out, FY27 consensus sits at roughly $14.04 per share, which would bring the forward P/E down to approximately 45 times on FY27 numbers — still premium, but within shouting distance of peers if growth continues. Revenue projections tell a similar story of rapid multiple compression: from $2.9 billion in FY26 to $4.62 billion in FY27, a 59% growth rate that would make the current EV/Sales multiple look far more reasonable in twelve months' time. The argument, in essence, is that you are paying 84 times this year's earnings for a company that may be earning $14 per share next year.

The problem is that "may" is doing enormous work in that sentence. Analyst price targets range from a high of $945 to a low of $385.03, with a median of $633.42. At a current price of approximately $625, Lumentum is trading essentially at the median target, which means the market is already pricing in the base-case outcome. The NVIDIA investment de-risks the balance sheet and validates the technology, but it does not de-risk the multiple. At 84 times forward earnings, any shortfall on the $780-830 million Q3 revenue guide, any delay in InP capacity coming online, any softening in hyperscaler CapEx sentiment would trigger severe multiple compression. A stock priced for perfection must deliver perfection, and the history of semiconductor and optical component companies suggests that perfection is an unreliable companion.

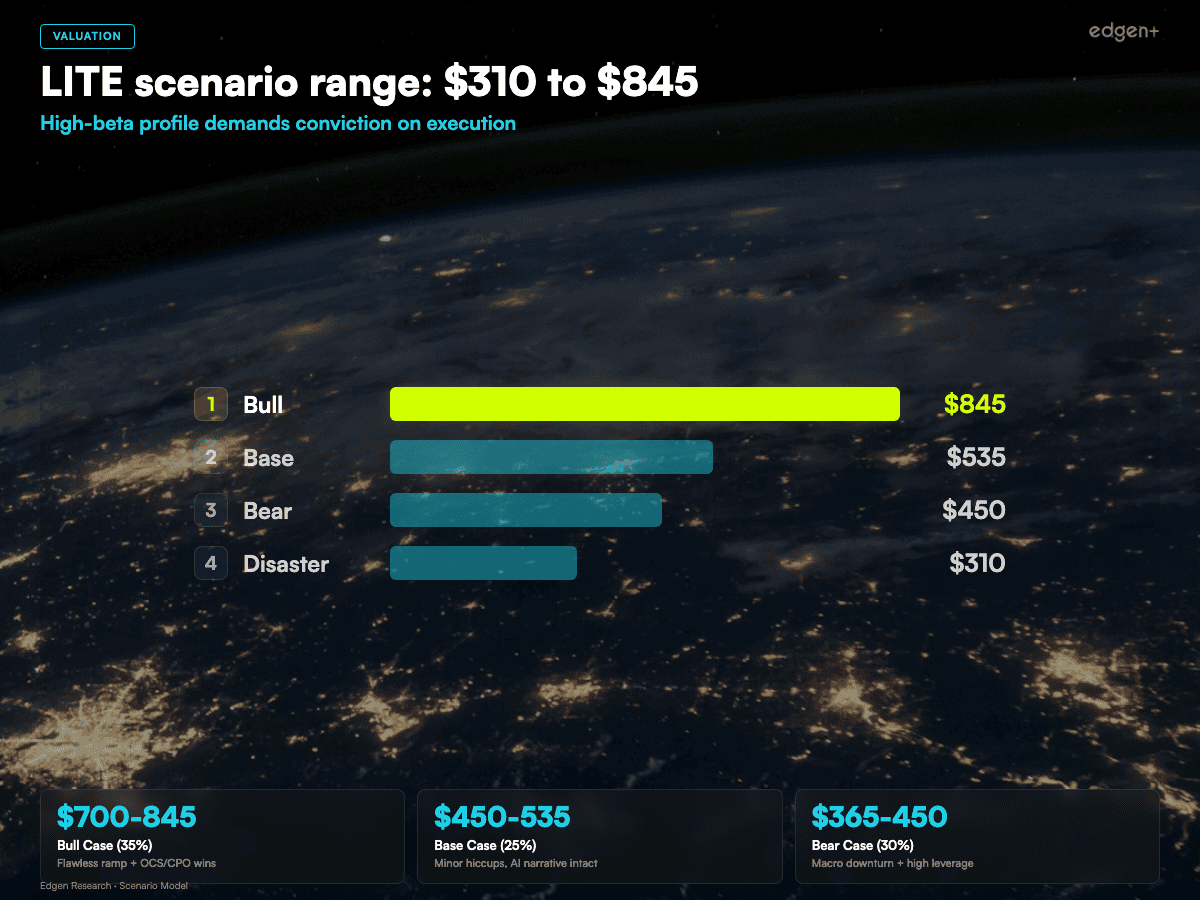

Three Scenarios

Scenario | Price Target | Market Cap | Probability | Key Assumption |

**Bull** | $700-845 | $50-60B | 35% | Flawless capacity ramp + OCS/CPO design wins + macro favorable |

**Base** | $450-535 | $32-38B | 25% | Minor operational hiccups, AI narrative intact but expectations disappoint |

**Bear** | $365-450 | $26-32B | 30% | Macro downturn + high leverage concerns despite NVIDIA backstop |

**Disaster** | <$310 | <$22B | 10% | Material execution failure + hostile macro |

Source: Edgen Research estimates. LITE three-scenario valuation.

Risks and Bear Case

Valuation Risk at 84x Forward P/E. The most immediate and quantifiable risk is the multiple itself. At 84 times forward earnings, Lumentum is priced not merely for strong growth but for sustained, flawless execution over multiple years. Coherent and Corning offer meaningfully similar exposure to the AI optical infrastructure theme at forward P/E multiples of 48.5 and 49 times respectively, meaning investors can participate in the same secular trend at roughly half the valuation risk. History is instructive here: optical component companies that traded at extreme multiples during the 2000 telecom buildout and the 2017-2018 3D sensing cycle experienced drawdowns of 30% to 70% when growth merely decelerated, even before turning negative. A single quarterly guidance miss at these levels — even a modest one where revenue comes in at $760 million versus the $780 million low end of guidance — could reasonably trigger a 20-30% correction as the market reassesses the premium.

Operational Execution on Capacity Ramp. Lumentum is simultaneously expanding indium phosphide wafer fabrication capacity across facilities in the United States, United Kingdom, and Japan. This is not a trivial manufacturing challenge. InP epitaxial growth and processing require extraordinarily tight yield controls, and new fab lines typically take 12-18 months to reach mature yields. Management has acknowledged that demand currently outstrips supply by approximately 30%, which means the company is leaving hundreds of millions of dollars in potential revenue on the table. Bringing that capacity online on schedule and at acceptable yields is the single most important operational variable in the model. Any delay — whether driven by equipment delivery timelines, yield issues, or labor constraints — would simultaneously disappoint on revenue while inflating per-unit costs, creating a double negative on earnings that the current valuation cannot absorb.

Customer Concentration in Hyperscalers. Lumentum's revenue is increasingly concentrated in a small number of hyperscale cloud providers, with the top three customers likely accounting for more than 50% of Cloud and Networking segment revenue based on the company's disclosure patterns. While the NVIDIA strategic partnership mitigates the risk of losing a single critical customer, it does not eliminate the binary nature of hyperscaler spending cycles. These customers make capital expenditure decisions in large, lumpy increments, and a single budget reassessment at Microsoft, Meta, or Google could remove hundreds of millions of dollars from Lumentum's near-term revenue trajectory. The strategic partnerships provide visibility into design wins, but they do not guarantee purchase order volumes in any given quarter, and the history of optical suppliers to hyperscalers is littered with companies that confused design wins with durable revenue streams.

Conclusion and Price Target

Lumentum is, without question, the most compelling growth story in the AI optical supply chain today. The combination of 65.5% revenue growth, a $2 billion NVIDIA strategic investment, imminent S&P 500 inclusion, a backlog exceeding $400 million in OCS alone, and a technology portfolio spanning 3,100-plus patents positions the company at the center of the most important infrastructure buildout since the original internet backbone. CEO Michael Hurlston has executed a remarkable strategic pivot in barely a year, transforming a struggling telecom component maker into a vertically integrated AI infrastructure platform that the world's most valuable chip company has chosen as its preferred optical partner.

But at approximately $625 per share with an 84 times forward P/E multiple, the stock is priced for a future that must unfold almost exactly according to plan. We rate Lumentum a Hold with a price target of $633, which aligns closely with the median analyst consensus and implies negligible upside from current levels. The risk-reward is asymmetric in the wrong direction at this price: the bull case offers perhaps 10-35% upside to the $700-845 range, while the bear case presents 25-40% downside to $365-450 on any meaningful execution stumble. For investors without an existing position, we would recommend patience — waiting for either a 15-20% pullback that provides a genuine margin of safety, or for the Q3 FY26 earnings report in early May 2026 to confirm revenue at or above the $805 million midpoint and operating margins at 30% or better.

One thing to watch above all else: the Q3 FY26 earnings call, expected in early May 2026. This is the single most important near-term test of whether Lumentum's growth trajectory justifies its premium valuation. If the company delivers $800 million or more in quarterly revenue with 30-plus percent operating margins and raises full-year guidance, the bull case to $845 becomes credible and the stock likely breaks to new highs. If it merely meets guidance without raising, the market will begin to question whether peak growth rates are behind us. And if it misses, even modestly, the 84x multiple will compress rapidly and painfully. At this valuation, there is no room for ambiguity.

Internal Links

- LITE Stock Forecast and Price Target

- COHR Stock Analysis: The AI Optical Supercycle

- AI Optical Sector Deep Dive: COHR vs LITE vs GLW

Frequently Asked Questions

Is LITE stock a good buy right now?

Lumentum is rated Hold. The company is delivering explosive revenue growth of 65.5% year-over-year and has secured a transformative $2 billion NVIDIA investment, but the stock trades at 84 times forward earnings, which prices in near-perfect execution. At approximately $625 per share, the risk-reward favors waiting for either a 15-20% pullback or confirmation from Q3 FY26 earnings that the growth trajectory is sustainable at these elevated expectations.

What is Lumentum's price target for 2026?

Our price target is $633, which aligns with the median analyst consensus. The full analyst range spans from $385 at the low end to $945 at the high end. Our bull case scenario targets $700-845 if the company delivers flawless capacity execution and secures additional OCS and CPO design wins in a favorable macro environment, which we assign a 35% probability.

Why did NVIDIA invest $2 billion in Lumentum?

NVIDIA invested $2 billion in convertible preferred stock to secure Lumentum as a preferred co-development partner for optical interconnects in its silicon photonics ecosystem. The investment supports NVIDIA's Spectrum-X Ethernet and Quantum-X InfiniBand networking platforms, which require high-performance optical components that few suppliers can produce at scale. This is a strategic supply chain partnership, not a passive financial investment.

How does LITE compare to COHR?

Lumentum is growing significantly faster than Coherent — 65.5% revenue growth versus approximately 17% for COHR — but trades at roughly double the valuation, with an 84x forward P/E compared to Coherent's 48.5x. Coherent offers better value and lower downside risk for investors seeking exposure to the AI optical infrastructure theme, while Lumentum offers higher beta and greater upside potential if execution remains flawless. The choice depends on individual risk tolerance and conviction in the sustainability of Lumentum's growth premium.

What are the biggest risks for LITE stock?

The three primary risks are valuation compression (at 84x forward P/E, any guidance miss could trigger a 20-30% correction), operational execution (simultaneously ramping InP fabrication capacity across three countries carries meaningful yield and timeline risk), and customer concentration (revenue is heavily dependent on a small number of hyperscale cloud providers whose capital expenditure cycles are inherently lumpy and unpredictable).

Not financial advice. For educational and research purposes only.

Recommend